Classic Car Quote Guide (May Include Progressive)

Classic and collectible vehicles often need a different insurance approach than daily drivers. This guide explains what to prepare before requesting quotes and what to compare for classic cars—especially mileage limits, storage requirements, deductibles, and how vehicle value is handled. Availability and coverage terms vary by state and provider, so always confirm details on the quote.

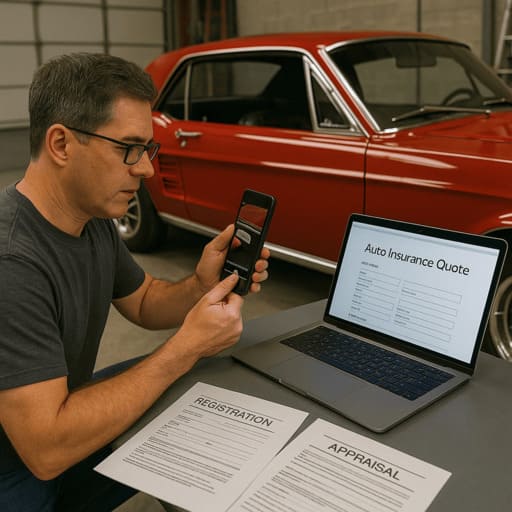

Use the steps below to collect the right information (photos, receipts, appraisals, and usage details). Then compare quotes with one consistent baseline (same ZIP code, drivers, limits, and deductibles) so pricing differences reflect real value—not different coverage settings.

Steps to Compare Classic Car Quote Options

Before requesting quotes, gather your vehicle’s make, model, year, and details about restorations or modifications. It also helps to document how the car is stored (garage, secured storage) and how often it is driven. These inputs can affect eligibility and pricing for classic or limited-use policies.

Get Your Auto Insurance Quote

Compare classic-car-friendly quote options by ZIP code and verify coverage terms in the details.

Explore Home Insurance Options

If bundling is available, compare the total annual cost against standalone quotes.

How to Start a Classic Car Quote Comparison

Once you have documentation ready, compare quotes using the same baseline configuration first (limits, deductibles, and usage). Many classic policies ask about annual mileage and storage because collectible vehicles are often driven less and stored more securely than daily-use cars.

If you want your comparison to include Progressive, you can start with Progressive quote comparison guide and then verify classic-car-specific terms in the coverage details. Keep in mind that classic policies can differ substantially from standard auto coverage.

If your vehicle is used only occasionally or seasonally, make sure your usage details are consistent across every quote. For seasonal driving patterns, see this seasonal driving coverage guide to avoid mismatched assumptions.

Understanding Coverage Options for Classic Cars

Classic car coverage often emphasizes how vehicle value is handled, what qualifies as covered usage, and whether repairs must be performed by specialty shops. Some policies may offer agreed value or similar valuation approaches, but availability and terms vary—so confirm what your quote specifies.

Other common considerations include limited-use rules, mileage allowances, storage requirements, and how aftermarket parts or restorations are treated after a loss. Review exclusions closely so you understand what is and is not covered.

If you have prior incidents on your record, focus on matching coverage settings first, then compare deductibles and optional protections one change at a time. You can also review: coverage guidance for drivers with prior accidents.

Frequently Asked Questions

What is the difference between classic car insurance and standard auto insurance?

Classic or collectible coverage may use different valuation methods, usage rules, and repair terms than standard policies. Always confirm what your quote states for value and usage.

How can I determine the value of my classic car?

A certified appraisal and documentation (receipts, photos, restoration records) can help support valuation. Some quotes may also reference valuation guides depending on provider rules.

Can I insure a classic car that I only drive occasionally?

Yes, many drivers compare limited-use configurations where available. Verify mileage allowances, storage requirements, and any usage restrictions on the quote.

Final Notes

Classic car quote comparisons work best when you prepare documentation, match baseline settings across providers, and verify how value and usage are handled. Once you have two or three comparable offers, choose the option that best fits your coverage goals and risk tolerance.

Next step: run a ZIP-based quote comparison above, then review the coverage details line by line before choosing any policy.